Knowledge Library

Insights

From Connection to Conversion: How Omnichannel Marketing Can Boost Brand Loyalty & Drive Revenue

Read this eBook where we take you through an overview of Omnichannel Marketing, the changes in consumer behavior & how you can meet these new demands, and an Omnichannel Marketing Checklist to ensure success.

Videocasts

Creating Brand Loyalty with Experiential Rewards & Events

During our upcoming webinar on April 23rd, Creating Meaningful, Memorable, and Motivating Brand Loyalty with Experiential Rewards & Events, 360insights’ experts will share insights and best practices for designing travel programs that inspire and motivate, while also delivering measurable business results.

Videocasts

Events

The Era of Ecosystem Orchestration is (Nearly) Here

Join us to learn how the best companies in the industry are coming together to provide the first integrated solutions stack to drive unparalleled Ecosystem scale and success. Save your seat!

Videocasts

Events

Growing Partner Mindshare in a Tumultuous Environment

Join 360insights' own Heather K. Margolis as she meets with the best and brightest for this On-Demand session, Growing Partner Mindshare in a Tumultuous Environment, to learn how to build programs that resonate with partners, motivate them to take action, and foster long-term engagement. Uncover the psychology and behavioral science behind partner mindshare, explore strategies to help partners understand the value of your programs and what’s in it for them, and ensure that you’re adapting your programs to keep partners interested and engaged over time.

Infographics

Your Rate Card Implementation Checklist

Read this infographic to learn more about what Rate Cards are and why you should be using them, a checklist for your successful creation and implementation of Rate Cards and what you should be doing after your program is up and running.

Infographics

The 5 Criteria of Successful Rate Card Program

Learn more about what a Rate Card is, the benefits of using a Rate Card, and the criteria you should follow for success.

Insights

The Definitive Guide for an Effective Channel Incentive Program

Read this eBook where we take you through 6 areas of focus that will help you run your incentive programs correctly and efficiently.

Videocasts

Driving Marketing Success in the EV Revolution: Strategies for Digital Dominance

Watch as we explore the impact of increasing budgets on impression share, the importance of keeping pace with digital trends, and maximizing reach in the digital space. Learn how to craft effective marketing strategies that resonate with EV consumers and dealers alike.

Insights

(Auto) The Not-so Secret Value of Consumer Rebates & Cashback Programs

Leveraging effective promotional strategies is crucial for success. One such strategy proven to be powerful is using rebates and cashback programs. These programs not only drive sales but also offer an opportunity to collect valuable customer data, enabling businesses to make informed decisions. Read to learn more

Infographics

The Not-So Secret Value of Consumer Rebates & Cashback Programs

Leveraging effective promotional strategies is crucial for success. One such strategy proven to be powerful is using rebates and cashback programs. These programs not only drive sales but also offer an opportunity to collect valuable customer data, enabling businesses to make informed decisions. Learn more by reading now!

Videocasts

Tiffani Bova and 360insights Help you Unlock Growth Potential Across your Business

Watch Tiffani Bova and 360insights as we help you unlock growth potential across your business.

Videocasts

Is it an Ecosystem? A Channel? A Partnership: Cut through the semantics and demystify the evolution to drive more revenue

During this on-demand replay, gain a deeper understanding of the nuances, and how they can drive revenue, expand market reach, and foster long-term customer relationships.

Videocasts

Making Your Partners Demand Generation Machines: How to Truly Enable Your Ecosystem

Watch our expert panelists to learn how to leverage new and different strategies to better educate, engage, and enable your ecosystem!

Videocasts

Unlocking Success: Expert Insights on Promotions in the Consumer Durables Industry

Fill out the form for an insightful webinar exploring the world of promotions in the consumer durables industry. This engaging session will feature a distinguished panel of experts, including Zack Elkin, President at Beko, John Iacoviello, former SVP Sales at B/S/H Home Appliance, Sharon Maxfield, Sr. Product Marketing Manager at 360insights and moderated by Heather Margolis, SVP of Marketing at 360insights. Together, they will dive deep into the strategies and tactics that make promotions successful, as well as those that fall short.

Videocasts

Are Marketplace REALLY Working for Your Business?

Watch our on-demand webcast with special guests Jay McBain, Chief Analyst at Canalys and Louise McEvoy, Vice President, US Channel at Trend Micro, where we'll delve into actionable ways to achieve true marketplace mastery.

.png?width=992&height=620&length=992&name=CMAR-636_Webinar_Get-Stuff-Done-Faster_Thumbnail-(552x350).png)

Videocasts

Get Stuff Done, Faster: Leveraging Analytics to Optimize Your Ecosystem

"So much to do, so much opportunity, so little time.” It’s a tale as old as partner ecosystems and an all too familiar phrase for overextended partner managers. Watch the On-Demand Replay to learn how you can leverage analytics to optimize your ecosystem!

Videocasts

This Is Not Your Grandparent’s Partner Enablement

This on-demand 360insights webinar will look at things you should be doing completely different and how you should be developing an enablement strategy, to truly engage and enable your partners. Watch now!

Videocasts

The Evolving Aftermarket Industry: Fine Tuning Consumer Promotions & Dealer Incentives

During this on-demand webinar, we explore the latest trends in the automotive industry, examining how factors like the rise of electric vehicles are impacting the industry, and what retailers need to know to serve this emerging market effectively. We'll also dive into consumer buying habits, with a particular emphasis on the role of access to credit and promotional offers in driving purchases and look at the role of incentives and promotions in the dealership environment.

.jpg?width=992&height=620&length=992&name=CMAR-684_Webinar_Ecosystem-Couples-Therapy_Gated-Thumbnail-(552-346px).jpg)

Videocasts

Ecosystem Couples Therapy: Ignite the Fire in Your Business Partnerships

Join 360’s SVP of Marketing Heather Margolis and SVP of Ecosystems James Hodgkinson for an on-demand webinar with Jay and Michelle McBain. They will tackle the common challenges that businesses face when managing ecosystems and explore how automation tools can be the ultimate counselor, streamlining processes and optimizing results.

Videocasts

Supercharging Your Channel Game with Generative AI

During this session, we'll dig into how generative AI is changing the channel landscape and how to help channel partners stay ahead of the curve. Don't miss this chance to understand how you can transform your channel strategy, and how to stay ahead of the competition.

Insights

The Shifting Automotive Aftermarket Landscape and the Moves Manufacturer and Reseller Brands Need to Make the Journey

Download this eBook where we dive into the current landscape, the shifts you need to know about, and your next five strategic plays.

Help Sheets

The Benefits of Instant Rebates vs. Consumer Rebates

Read this help sheet where we explore the key considerations when choosing between instant vs consumer rebates.

Videocasts

Uncertain Times, Certain Success: Leveraging Demand Generation to Help Channel Partners Flourish

Do your partners have what they need to succeed? Watch our star-studded panel from all facets of the channel talk through challenges and strategies.

Case Studies

Technology: Matillion Maximizes Partner Pipeline

Learn how data integration company Matillion are maximizing partner business opportunities and mutual bottom lines by supporting partners

Case Studies

Automotive: Manufacturer Polaris implements high impact dealer portal

Learn in this Case Study how, Polaris International designed and implemented a high impact dealer portal offering a unique experience for their diverse international dealer community and portfolio of off-road and on-road products. One that has the ability to deliver relevancy and enriching experiences to all dealers – whatever their location, type and time zone!

Help Sheets

API vs. SFTP with Single Record and Bulk Records and Recommended Frequencies

This help sheet delves into the pros & cons of each approach, & discusses how the choice of data integration method impacts reporting and visualizations.

Videos

Navigating the Entrepreneurial Journey: Overcoming Challenges and Building Authentic Connections

Join Kathryn Rose, Founder and CEO of Get Wise and Channel Wise and Heather Margolis, the SVP of Marketing for 360insights for a candid and thought-provoking conversation about the realities of entrepreneurship.

Insights

Beyond PRM: Rethinking the Tech Stack for Ecosystem Orchestration

Building a modern, strong tech stack is crucial for businesses to stay relevant in an ecosystem-focused world and expand their reach. It allows organizations to leverage advanced technologies, streamline operations, and integrate various tools and platforms to effectively manage and orchestrate their ecosystem interactions. But what does this tech stack look like and how does it differ from tech stacks of the past? Read this eBook to find out more.

Videos

Transforming & Modernizing Consumer Incentives Programs

In this video, 360insights' Kelsey Anderson reflects on key highlights and tips to consider for building an effective consumer incentives strategy.

Case Studies

Manufacturing: Hoover Points-Based Reward Incentives

Working with 360insights Hoover implemented an online B2B sales points-banking incentive and rewards program that boosted sales growth. See the results

Videos

Leveraging Incentives for Financing Solutions & Retail Credit Cards

In this video, 360insights' Kelsey Anderson discusses how incentives are being leveraged by financial solutions for retail credit card offers.

Videos

Current Automotive Industry Insights & Incentives Trends

In this video, Kelsey Anderson discusses what is happening on the dealership & retailer sales floors, including preserving the life of a vehicle.

Videos

Being Mindful of The Modern Consumer Rebate Experience

Kelsey Anderson outlines how to coach brands who are launching or looking to reimagine their consumer incentives programs to always prioritize CX.

Videos

Personifying Consumer Incentive Programs To Meet Your Go to Market Business Objectives

Kelsey Anderson discusses how B2C brands can align their go-to-market business objectives and bring goals to life in how consumer programs are executed.

Videos

Push/Pull & Cross Program Consideration

In this video, Sharon Maxfield, Senior Manager Product Marketing at 360insights, shares key observations from B2B routes to market.

.png?width=992&height=620&length=992&name=360-buildbuy_Hubspot-Thumbnail-(552-346px).png)

Infographics

Build vs. Buy: Channel Incentives Management Platforms

This infographic shows the top 3 considerations in the build vs. buy debate, so you can narrow down a “winning” solution that’s right for your business.

Videos

Helping Partners Become Recognized Industry Influencers

In this video, Heather K. Margolis and PR expert CJ Arlotta explore why executive and channel partner thought leadership should be a top priority for businesses right now.

Insights

Reports

Consumer Durables in the Post Pandemic Era: A Renaissance Journey

We conducted research to try to learn what consumer durables businesses priorities are and how they are preparing for the next 6-12 months and beyond. Read now to learn what insights came from our research.

Videos

Applying Personalization & Profiling in & For Your Ecosystem & Incentives

Sharon Maxfield emphasizes the importance of profiling a brand's ecosystem and using incentive programs to align with core business objectives.

Videos

Incentives Automation for Your Ecosystem

Ecosystem incentivization goes beyond behavior modification and extends to increased adoption of programs and tooling for go-to-market personas.

Help Sheets

Consumer Incentives: Gift with Purchase vs Cash Incentives

Read this help sheet for key considerations when choosing between gift with purchase and cash incentives.

Videos

What is Gamification

Sharon Maxfield suggests ways to add a personalized touch within programs to increase engagement and enhance the effectiveness of incentives.

Videos

Putting Incentive Automation in Action

Sharon Maxfield highlights the importance of incentives automation in offering program options to a brand's ecosystem.

Videos

B2B Rebate Trends

B2B Rebates for the Technology, Media & Telecom industry involve transactional, calculated, and subscription-based rebates with different purposes.

Videos

Who, Why & How You Incentivize & The Buyer’s Journey

Sharon Maxfield highlights key areas where brands often miss out on opportunities to include persona-based incentives that can impact the sales lifecycle.

Case Studies

Manufacturing: Danby Accelerating Performance with SPIFFs

Learn how Danby appliances implemented a strategic SPIF program to drive customer behaviors to increase performance across brand loyalty and sales.

Case Studies

Automotive: Manufacturer Full Stack Channel Incentive

Read how, with the help of 360insights, an Automotive Manufacturer was able to influence dealer channel behavior, and gain a better attribution of direct program ROI.

Videos

Getting Creative & Strategic With Consumer Incentives

Sharon Maxfield discusses new ideas for consumer incentive programs that go beyond traditional consumer rebates as B2C go-to-market initiatives expand.

Videos

Flexibility & Strategy Through Co-Op MDF Funds Management

Sharon Maxfield discusses how brands can use gamification to diversify their co-marketing programs beyond just sales incentives in Co-Op/MDF programs.

.jpg?width=992&height=620&length=992&name=CMAR-502-Tacking-Against-WP_Thumbnail-(552x346px).jpg)

Reports

Tacking Against the Headwinds: 2023 State of Channel Incentives Report

According to our latest research, incentives are proving resilience against economic downturns. Learn how incentives are helping brands weather the storm, enable greater success, and generate support for partners, dealers, and resellers alike in 2023 and beyond.

Help Sheets

360insights Health Plans Help Sheet

Read this Help Sheet to see how an automated Incentives and Rewards platform improves HEDIS scores while helping you go the extra mile to engage and serve your members.

.png?width=992&height=620&length=992&name=Q4-Pillar-Socials-Promo2_Thumbnail-(552x346px).png)

Insights

Navigating The C's of Unpredictability

Supply chain disruption, manufacturing shortages, labor issues, and rapid market changes have made setting the right mix of incentives and rebates even more challenging. Learn how the right incentive management platform can offer flexible and dynamic solutions that intelligently manage and optimize your channel incentives.

Videos

Technology Partnerships

In this video, Heather K. Margolis, SVP of Marketing at 360insights is joined by Kelly Sarabyn, Platform Ecosystem Advocate at HubSpot to discuss the importance of partnerships, the evolution of HubSpot's partnership programs, and tips for growing partner ecosystems.

Videos

Business Travel Tips

In this video, Heather K. Margolis, SVP of Marketing at 360insights is joined by Rachel Schaeffer, Global Director of Channel for Strategic Alliances at SuccessKPI to discuss tips and tricks for managing intense business travel schedules.

Events

Channel Focus Virtual: April 17-18

Join virtually on April 17-18, 2024 for live sessions, interactive Q&A, and one-on-one meetups. Channel Focus, shaping Channel trends for 25 years, offers strategic, best practice, and tactical presentations.

Events

AHTD Spring Conference: April 17-19

Come join us in San Antonio, Texas for AHTD’s Spring Meeting 2024, scheduled for April 17-19, 2024 at the JW Marriott Hill Country Resort. AHTD looks forward to greeting friends--old and new--at the Welcome Reception on Wednesday, learning about new member offerings at our signature Product Showcase Reception on Thursday, and celebrating at the final night party! Plan to stay over Friday, April 19 to take part.

Events

Extreme Connect 2024 User Conference: April 22-25

Come to the biggest Extreme event of the year to experience the deep intersection of AI, security, and cloud networking and what it means to the future of business. This four-day event in Fort Worth, Texas, is packed with inspiring speakers, exciting activities, and immersive sessions. Don’t forget to register!

Events

Kaseya Connect: April 29-May 2

Kaseya Connect Global is designed for leaders and experts in the IT service industry looking to help build systems, evolve their companies, and help lead the industry into a stronger tomorrow.

Events

The Special Needs Plan Leadership Summit: May 1-3

Bring your whole team to the ONLY non-association conference focused on SNPs that brings together health care leaders charged with maximizing plan resources for improving patient outcomes through new CMS audit protocols and integration, marketing and operational strategies, plus compliance and audit readiness benchmarks.

Events

Forrester B2B Summit North America: May 5-8

B2B Summit North America is coming to Austin May 5 – 8, 2024. It’s where thousands of your peers are headed — to discover how to accelerate profits and growth by amplifying the value you bring to customers.

Events

B2B Online: May 6-8

B2B Online stands as the premier 3-day event tailored for B2B professionals within the manufacturing and distribution sectors, all with a keen interest in bolstering their eCommerce, omni-channel, and digital marketing prowess.

Events

RSA Conference 2024: May 6-9

Join us in cheering on these ten trailblazers as they redefine the future of cybersecurity. Don't miss out on this opportunity to witness innovation in action! Plus, it's the final week to save $600* on a Full Conference Pass. Secure your spot now and be part of the excitement at RSAC 2024!

Events

UK Construction Week London: May 7-9

Join 300+ of the Biggest Brands in Construction gathered in London!

Events

IMEX GERMANY: May 14-16

IMEX is where every part of the global events industry comes for a high-value, high-return boost of real business, real relationships and insights, all designed to make working life easier and more profitable.

Events

Dentistry Show: May 17-18

Understanding the importance of the entire dental team is a core value at the British Dental Conference & Dentistry Show (BDCDS). You know more than anyone that each role, inside or outside the practice, feeds into the end goal; giving patients the best treatment possible. Unite with your peers at BDCDS and build a better future for the profession together.

Events

CFMA’s Annual Conference & Exhibition: May 18-24

Continue your path to bigger and better education, leadership, networking, and connections at CFMA’s 2024 Annual Conference & Exhibition in Texas on May 18-22! Immerse yourself in a wealth of essential educational sessions, forge meaningful connections with industry peers, and explore cutting-edge product offerings critical to your success.

Events

Dell Technologies World: May 20-23

Dell Technologies World – happening at The Venetian in Las Vegas, May 20–23, 2024 – is a showcase of all the ways we’re using technology and AI to accelerate from ideas to innovation. Meet up with a community of technologists and innovators to share stories, understand our vision for the future and be a part of what’s next.

Events

NAED: May 21-23

Industry-leading companies from around the country gather together for the National Meeting to network, learn about business trends, and listen to world-class speakers.

Events

Qualipalooza: The RISE Quality Leadership Summit: June 2-4

Qualipalooza, THE leading ‘teamcentric’ conference, is focused on quality of care and improving member experience. We have curated content that caters to organizational interdisciplinary teams with a stake in quality improvement and member touchpoints in the health care journey.

Events

The RISE Value-Based Care Summit: June 3-4

As the only conference in the market that joins together payers and providers in the same setting, The RISE Value-Based Care Summit bridges the gap in the care continuum to reveal the roadmap to value-based health care delivery. This event brings together mid- to senior-level professionals from health plans, health care providers, medical groups, accountable care organizations (ACOs), employer groups, and service providers to uncover new strategies to align financial incentives, improve patient outcomes, and better navigate the value-based care space.

Events

Gartner Marketing Symposium Expo. June 3-5

Attendees explore the latest marketing trends, emerging technology and more at Gartner Marketing Symposium/Xpo™ 2024, in Denver, CO.

Events

IT Nation Secure 2024 Conference: June 3-5

IT Nation Secure is the IT industry’s must-attend cybersecurity event to help you reduce risk, transform your business, and streamline service delivery of cybersecurity solutions for your clients.

Events

SubCon [Manufacturing Mgmt Show/Engineering Expo]: June 5-6

Subcon (5-6 June 2024 | NEC) is the must-attend event for manufacturing buyers across all industry sectors. Discover an expected 150+ subcontract and outsourced engineering services alongside a dynamic content programme. Join interactive CPD-accredited workshops, product demonstrations, keynote presentations, roundtable discussions, and much more.

Events

Autotech: June 5-6

AutoTech: Detroit gathers 3,000+ industry stakeholders for two days of focused B2B networking.

Events

Med-Tech Innovation Expo: June 5-6

Med-Tech Innovation Expo event brings together leaders, engineers, innovators and manufacturers, connecting them with technology and innovation to facilitate the design and manufacture of life changing medical devices.

Events

IoT and Tech: June 5-6

IoT Tech Expo is the leading event for IoT, Digital Twins & Enterprise Transformation, IoT Security IoT Connectivity & Connected Devices, Smart Infrastructures & Automation, Data & Analytics and Edge Platforms.

Events

London Tech Week: June 10-14

Innovators. Investors. Tech giants. The visionaries applying new tech to solve the world’s biggest problems. Enterprise tech leaders who are creating solutions to enrich every aspect of our lives. They all come to London Tech Week to see where tech will take them next.

Events

Digital Enterprise Show: June 11-13

Buy your tickets now to attend DES2024, the largest event on exponential technologies.

Events

AHIP 2024: June 11-13

Experience what’s next in health care at AHIP 2024 (Formerly Institute & Expo). We’re building on AHIP’s decades-long heritage of bringing together the people, ideas, and solutions guiding greater health for years to come.

Events

Connected Manufacturing Forum: June 18-19

oin 200+ leading Manufacturing, Operations, Technology, Supply Chain and Advanced Engineering executives for a collaborative debate on the latest Industry 4.0 (& 5.0!) trends, challenges and opportunities.

Events

The Installer Show: June 25-27

Every year, InstallerSHOW features the industry’s biggest names alongside up-and-coming brands and brand new businesses – all there to showcase the latest heating, plumbing and electrical products and services. It’s your chance to see the latest trends and stay up to date.

Events

The Optimizing Appeals and Grievances Summit: June 25-26

Featuring two days of immersive insight and instruction, the Optimizing Appeals and Grievances Summit is a can’t-miss opportunity for all compliance specialists looking to improve ODAG & CDAG outcomes.

.png?width=992&height=620&length=992&name=Blog_Flipping%20Supply%20Chain%20Issues%20On%20Their%20Head_Thumbnail%20(552x%20346).png)

Flipping Supply Chain Issues On Their Head

Flipping Supply Chain Issues On Their Head

.png?width=992&height=620&length=992&name=Blog_Shifting%20Supply%20Chains%E2%80%A6Help%20Sales%20Teams%20Do%20More%20with%20Less_Thumbnail%20(552x%20346).png)

Shifting Supply Chains…Help Sales Teams Do More with Less

Learn how brands are helping sales teams do more with less by optimizing manufacturing, inventory, distribution, and resale processes to maintain time to market, partner engagement and loyalty!

.png?width=992&height=620&length=992&name=Blog_Recession-Proof%20and%20Grow%20Your%20Channel_Thumbnail%20(552x%20346).png)

Recession-Proof and Grow Your Channel

Within a recession, businesses have every opportunity to engage their channel to keep sell-through opportunities alive and ensure partner loyalty and growth.

.png?width=992&height=620&length=992&name=Blog_5%20Tips%20to%20Drive%20More%20Revenue%20Through%20The%20IT%20Channel%20in%20an%20Economic%20Downturn_Thumbnail%20(552x%20346).png)

5 Tips to Drive More Revenue Through the IT Channel in an Economic Downturn

The reality is, rebates and incentives become MORE important during times of economic uncertainty. How you ask? Here are just a few reasons.

.png?width=992&height=620&length=992&name=Blog_5%20Things%20to%20Consider%20When%20Choosing%20the%20Right%20Channel%20Incentive%20Management%20Solution%20for%20Your%20Business_Thumbnail%20(552x%20346).png)

5 Things to Consider When Choosing the Right Channel Incentive Management Solution for Your Business

Here's 5 tips to drive behaviors, gain partner mindshare and influence customers through your Channel Incentive Management (CIM) solution.

.png?width=992&height=620&length=992&name=Blog_Top%20Performing%20Modern%20B2B%20Rebate%20Programs%20_Thumbnail%20(552x%20346).png)

Top Performing Modern B2B Rebate Programs

Learn how to support to channel partners by ensuring your B2B Rebate Program is simple, easily defined, clearly communicated, and effectively managed.

.png?width=992&height=620&length=992&name=Blog_Aligning%20the%20Buyer%20and%20Partner%20Journey_Thumbnail%20(552x%20346).png)

Aligning the Buyer and Partner Journey

The number one issue impacting channel brands and partners today is the misalignment of the partners’ sales process to the digitally connected buyer.

.png?width=992&height=620&length=992&name=Blog_How%20to%20Ensure%20Points-Based%20Incentive%20Programs%20Really%20Drive%20Sales_Thumbnail%20(552x%20346).png)

How to Ensure Points-Based Incentive Programs Really Drive Sales

Points-Based incentive programs are one of the most effective ways to drive dealer and distributor engagement, motivate revenue-generating behavior, and increase sales volume. Here's why.

.png?width=992&height=620&length=992&name=Blog_Enabling%20Partners%20with%20Through%20Channel%20Marketing%20Automation%20Awards_Thumbnail%20(552x%20346).png)

Enabling Partners with Through Channel Marketing Automation Awards

TCMA Awards combine marketing skills transfer and vendor-specific program information with incentives, to empower partners to execute vendor-created marketing.

.png?width=992&height=620&length=992&name=Blog_The%20Evolution%20of%20MDF_Thumbnail%20(552x%20346).png)

The Evolution of MDF

Discover our five best practices, that can be utilized to improve the effectiveness of your current or new MDF program.

.png?width=992&height=620&length=992&name=Blog_Why%20Your%20Sales%20Funnel%20Should%20Actually%20Be%20a%20Flywheel_Thumbnail%20(552x%20346).png)

Why Your Sales Funnel Should Actually Be a Flywheel

Here’s what you need to know about the sales flywheel, and how to incentivize channel partners and sales teams.

.png?width=992&height=620&length=992&name=Blog_4%20Ways%20to%20Eliminate%20Channel%20Partnership%20Friction%20Across%20the%20Entire%20Partner%20Lifecycle_Thumbnail%20(552x%20346).png)

4 Ways to Eliminate Channel Partnership Friction Across the Entire Partner Lifecycle

Learn more about what causes channel partnership friction and steps you can take to eliminate it throughout the entire sales process.

.png?width=992&height=620&length=992&name=Blog_Enhance%20Incentive%20Strategies%20and%20Sales%20Team%20Enablement_Thumbnail%20(552x%20346).png)

Enhance Incentive Strategies and Sales Team Enablement

If you’re like most, the tried and true sales incentive tactics you’ve relied on in the past just aren’t cutting it anymore. Here are a few easy ways to enhance incentive strategies.

.png?width=992&height=620&length=992&name=Press%20Release_360insights%20Named%20A%20Channel%20Incentives%20Management%20Leader%20By_Thumbnail%20(552x%20346).png)

360insights Named A CIM Leader By Major Independent Research Firm

New Report Gives 360insights Top Score in Strategy Category Within the Channel Incentive Management (CIM) Evaluation.

360insights’ Heather K. Margolis Joins Channel Development Advisory Council for CompTIA

360insights is excited to share that Heather K. Margolis, SVP Marketing, has been selected to join the Channel Development Advisory Council for Computing

.png?width=992&height=620&length=992&name=Press%20Release_360insights%20Named%20to%202022%20Lists%20of%20Best%20Places%20To%20Work%E2%84%A2_Thumbnail%20(552x%20346).png)

360insights Named to 2022 Lists of Best Places To Work™ in Canada and the United Kingdom

360insights announced that it has been recognized as one of Canada’s Best Places to Work™ for the tenth year, whilst UK ranks for the first time.

.png?width=992&height=620&length=992&name=Press%20Release_360insights%20Named%20a%202022%20UKs%20Best%20Workplaces%20for%20Women_Thumbnail%20(552x%20346).png)

360insights Named a 2022 UK Best Workplaces™ for Women

The 2022 UK’s Best Workplaces™ for Women list was launched this week by Great Place to Work® UK, recognizing 360insights among 263 ranked organizations.

Infographics

5 Steps To Achieve Ecosystem Orchestration

Ecosystems need to be built with orchestration in mind to create synergy across programs, platforms, and methodology, to ensure a seamless experience

Case Studies

Appliances: Using 360s Rebate Technology to Elevate Consumer Experience

360insights helped a client leverage the latest technology for a successful consumer rebates platform to elevate the consumer experience and drive sales.

.png?width=992&height=620&length=992&name=e-book_How%20incentivized%20learning%20can%20benefit%20your%20business_Thumbnail%20(552x%20346).png)

Insights

How Incentivized Learning can Benefit your Business

Discover how incorporating incentivized learning into your SPIFF strategy, will build loyalty, increase brand awareness and accelerate performance.

Infographics

The State of: Channel Incentives

This infographic explains why channel incentives are used and how they are successful, and some of the trends and challenges that they face in the future.

Infographics

The State of: MDF

This infographic will take you through why MDF & CO-OP programs are still so important, and what comes next for them in the ever changing channel.

Infographics

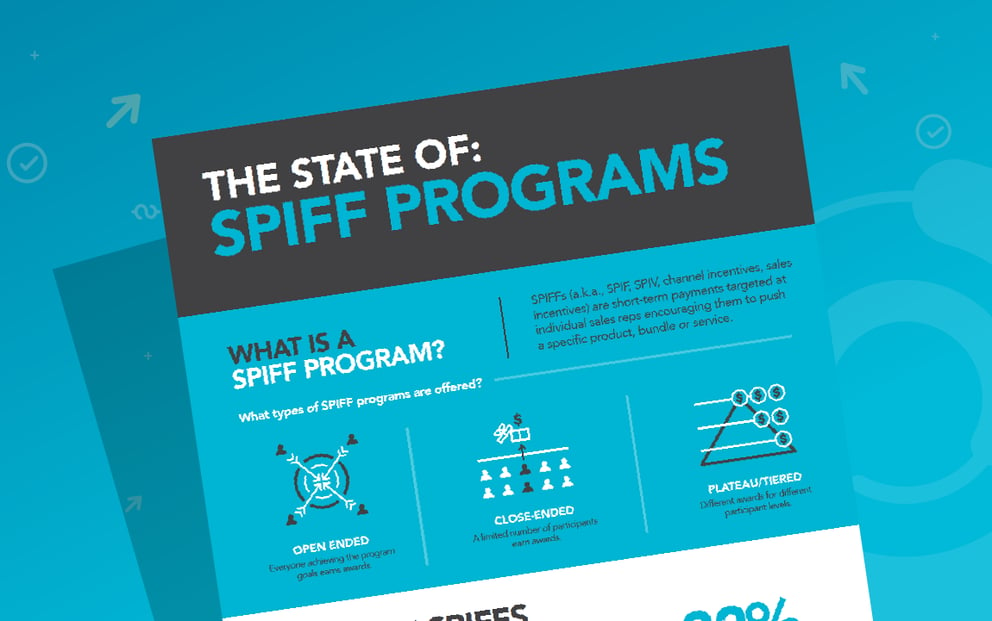

The State of: SPIFF Programs

Grow sales revenue and create connections between your channel and brand. This infographic defines SPIFFs and how to navigate SPIFFs.

Infographics

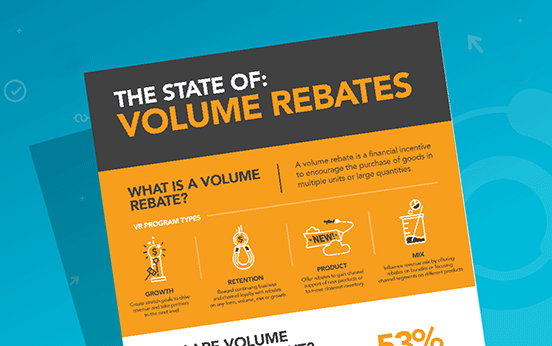

The State of: Volume Rebates

Volume Rebates (VRs) encourage the purchase of goods in large quantities for a financial incentive. This infographic defines VRs and how to navigate them.

Infographics

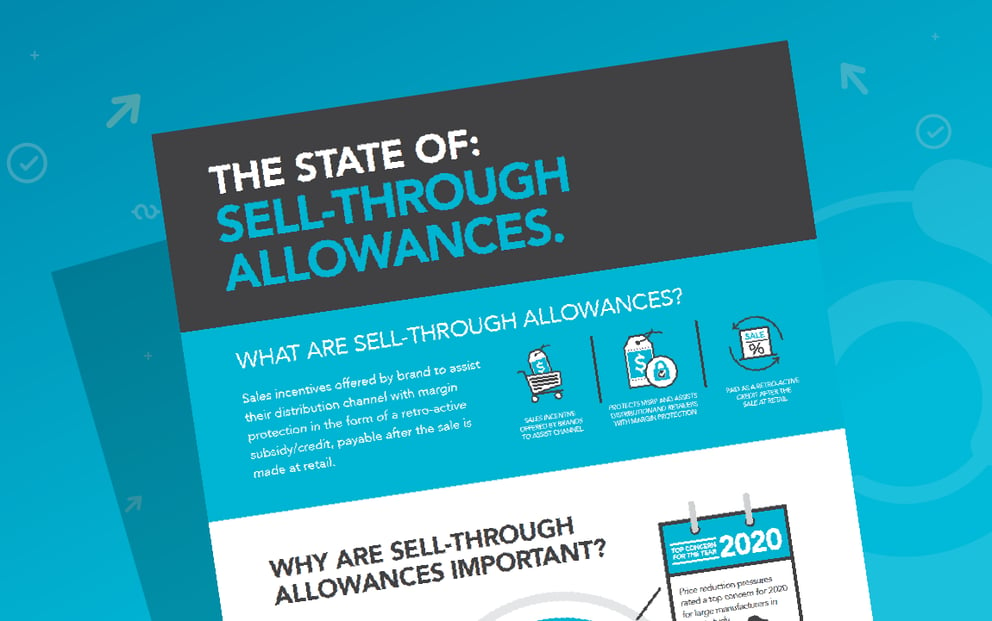

The State of: Sell-Through Allowances

Sell through allowances (STA's) offer retailer support retroactively while protecting MSRP. This infographic defines STA's and how to navigate them.

Infographics

The State of: Channel Insights

Channel insights bring brand confidence, channel efficiency and pipeline accuracy. This infographic defines channel insights and how to navigate them.

Infographics

Advantages of the 360insights SaaS Platform

360insights provides a customizable, secure, and efficient SaaS solution - The Channel Success Platform™.

Case Studies

Technology: Delivering outstanding ROI and global sales performance

This online points-based solution integrated partners globally, strengthened relationships and provided sales pipeline awareness for this IT Manufacturer.

.png?width=992&height=620&length=992&name=Reports_Forrester%20Thought%20Leadership%20Paper_Thumbnail%20(552x%20346).png)

Reports

Forrester: Elevate Your Partner Ecosystem Management

360insights commissioned Forrester Consulting to evaluate the importance of partner ecosystem management solutions amid the growing complexity of the channel.

%20copy.png?width=992&height=620&length=992&name=Videos_The%20360view%20-%20Cultivating%20and%20Managing%20Healthy%20Channel%20Ecosystems_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

The 360view - Cultivating and Managing Healthy Channel Ecosystems

Everyone is talking about ecosystems, and some of us longer than others, but how do you truly build an ecosystem that can thrive and grow?

%20copy.png?width=992&height=620&length=992&name=Videos_Optimizing%20Partner%20Engagement%20Series%20Part%203-%20Measuring%20Partner%20Engagement_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Optimizing Partner Engagement Series Part 3: Measuring Partner Engagement

Watch this discussion to gain insights into how you can measure engagement and help you identify areas where you can increase partner productivity.

Videocasts

Outperform your Competition

Adding the right incentive solutions can?amplify key enablement?efforts and further drive partner engagement. Watch the videocast to learn how.

%20copy.png?width=992&height=620&length=992&name=Videos_LinkedIn%20Live-%20Channel%20Wrap-Up%20-%20From%20Funnels%20to%20Fly%20Wheels_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

LinkedIn Live: Channel Wrap-Up - From Funnels to Fly Wheels

Understand how enhancements to partner engagement transitioning from traditional funnels to fly wheels will affect the future of the channel.

%20copy.png?width=992&height=620&length=992&name=Video_Optimizing%20Partner%20Engagement%20Webinar%20Series%20Part%202_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Optimizing Partner Engagement Webinar Series Part 2: Forrester Partner Engagement Framework

Channel leaders who tailor engagement strategies to partners will see relationships thrive. Follow these tips for an effective partner engagement strategy.

%20copy.png?width=992&height=620&length=992&name=Video_Webinar-%20Optimizing%20Partner%20Engagement_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Optimizing Partner Engagement Webinar Series: Part 1

View this videocast to learn the best practice recommendations for digital partner engagement, so brands can enable their partners to win business.

%20copy.png?width=992&height=620&length=992&name=Videos_360%20and%20IT%20Industry_Thumbnail%20(552x%20346)%20copy.png)

Videos

360 and IT Industry

Technology companies turn to technology solution providers, channel partners, MSPs and influencers to drive more revenue, but motivating and enabling your partners can be expensive, difficult to scale, and beyond challenging. Learn how 360insights can enable sales and increase ROI by delivering a modern and intuitive channel incentive experience.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_Baptie%20Webinar%20Automation%20-%20Is%20This%20the%20Key%20to%20a%20Successful%20Partner%20Program_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Baptie Webinar Automation - Is This the Key to a Successful Partner Program?

Learn how you can use automation and data insights, to enhance partner engagement and deliver a more personalized partner experience.

%20copy.png?width=992&height=620&length=992&name=Videos_Automated%20Automotive%20Industry%20Solutions-%20SimplyCast%20360_Thumbnail%20(552x%20346)%20copy.png)

Videos

360 and the Automotive Industry

Automotive and Tire companies can rely on service technicians to drive revenue through auto aftercare sales by incenting the behaviors that drive engagement.

Videos

Our Contribution to International Women's Day 2023

Watch this short video from Heather K. Margolis, Theresa Caragol, and Lisa Citron about International Women's Day 2023.

%20copy.png?width=992&height=620&length=992&name=360%20and%20the%20Kitchen%20&%20Bath%20Industry_Thumbnail%20(552x%20346)%20copy.png)

Videos

360 and the Kitchen & Bath Industry

Major Kitchen and Bath appliances companies rely on their dealer sales teams to drive revenue. Learn how to engage dealers to focus on your business.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_International%20Womens%20Day%20V-%20%20Post%20COVID_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

International Women's Day Videocast #1: Filling the Female Talent Void and Empowering Women to Re-Engage Post COVID

Learn how to engage and inspire female talent, by listening to this videocast. Understand how companies can connect, recruit, and empower women post-covid.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_Videocast-%20%E2%80%9CThe%20Shift%E2%80%9D%20-%20Helping%20your%20Channels%20and%20their%20Customers%20Overcome%20Inventory%20and%20Labor%20Shortages_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Videocast: “The Shift” - Helping your Channels and their Customers Overcome Inventory and Labor Shortages

Learn how to motivate, incent, and retain sales teams when they are overcoming inventory and labor shortages.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_IWD%202021%20Video_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

IWD 2021 Video

Listen to this informative discussion about how to achieve equality in the workplace, on International Women's Day 2021.

%20copy.png?width=992&height=620&length=992&name=Video_360%20Channel%20Success%20-%20UK_Thumbnail%20(552x%20346)%20copy.png)

Videos

360 Channel Success - UK

Learn how 360insights can help deliver a modern and intuitive partner experience to help sales people break through environmental complexities.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_International%20Womens%20Day%20Videocast%20Series%20%233-%20Mentors%20that%20Mean%20Something_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

International Women's Day Videocast Series #3: Mentors that Mean Something

Listen to this lively and informative discussion about what motivates women’s interest, brand loyalty and purchase decision making.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_International%20Womens%20Day%20Videocast%20Series%20%232-%20Selling%20to%20Women-%20Female%20Purchasing%20Power%20Has%20Evolved_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

International Women's Day Videocast Series #2: Selling to Women: Female Purchasing Power Has Evolved

Listen to this lively and informative discussion about what motivates women’s interest, brand loyalty and purchase decision making.

%20copy.png?width=992&height=620&length=992&name=Video%20Cast_Optimizing%20Partner%20Engagement%20Series%20Part%204-%20Case%20Study_Thumbnail%20(552x%20346)%20copy.png)

Videocasts

Optimizing Partner Engagement Webinar Series Part 4: Case Study

In 360's Optimizing Partner Engagement series, we bring you insights into how one of our clients has successfully optimized its channel success program.

Case Studies

Automotive: Stapletons - Points Based Reward Incentives

Customer loyalty points-based program, incentivizing UK tire resellers to purchase premium tire ranges & SKU's, driving sales growth & revenue.

Insights

Consumer vs. Instant Rebates: Which is Best?

Understand the differences between consumer and instant rebate programs, best practices, considerations & how they impact various target audiences.

Case Studies

Manufacturing: Fisher & Paykel Drive Sales

Fisher & Paykel, a manufacturer of kitchen and laundry appliances, worked with 360insights to launch new SPIFF and Consumer Rebate programs. See the results.

Case Studies

Technology: MDF & Co-Op Solution for Success

Read about how 360insights was able to implement a MDF & CO-OP program solution to help a fortune 50 international tech company reach success.

Insights

Elevating Consumer Rebates

This eBook lays out the proper methodology to enhance consumer rebate programs and optimize program spend, to ensure they reach their full potential.

Insights

The Essential Guide to Running Successful Sales Incentives

In this eBook 360insights explore the ways to connect with the sales channel, improve your sales incentive and enhance user experience.

.png?width=992&height=620&length=992&name=e-book_A%20Guide%20to%20Incentive%20Planning%20Selection_Thumbnail%20(552x%20346).png)

Insights

A Guide to Incentive Planning & Selection

In this eBook 360insights shares what to review when planning and selecting the right channel incentives, to ensure every member involved keep motivated.

-1.png?width=992&height=620&length=992&name=e-book_Sell-Through%20Allowances%20Reinvented_Thumbnail%20(552x%20346)-1.png)

Insights

Sell-Through Allowances Reinvented

In this eBook, 360insights provides benefits and challenges of sell-through allowances (STA) as well as how to leverage STAs to your advantage.

.png?width=992&height=620&length=992&name=Insentive%20Insights%202_Thumbnail%20(552x%20346).png)

Insights

360insights Auditor Checklist

This checklist will help you identify incentive fraud detection and empower you to better protect against fraudulent claims.

Insights

The Secret Ingredient to Partner Enablement

How vendors can improve the effectiveness of partners’ marketing enablement & develop marketing certification programs to improve performance.

.png?width=992&height=620&length=992&name=e-book_Guide%20to%20Getting%20Started%20with%20Channel%20Incentive%20Programs_Thumbnail%20(552x%20346).png)

Insights

Guide to Getting Started with Channel Incentive Programs

How to efficiently utilize time, budget & resources to produce a high performing innovative channel incentive program, delivering impactful ROI.

.png?width=992&height=620&length=992&name=e-book_10%20Essentials%20for%20a%20Successful%20MDF%20&%20CO-OP%20Marketing%20Program_Thumbnail%20(552x%20346).png)

Insights

10 Essentials for a Successful MDF & CO-OP Marketing Program

Understand how to plan, design and execute effective MDF & CO-OP programs that drive channel growth and deliver ROI.

Case Studies

Automotive: Apollo Vredestein Accelerates Customer Experiences

Apollo Vredestein increased end-user engagement and expanded into new buyer markets by centralizing and automating Incentives. Learn more

Insights

Building a Business Plan For Your Partners

Discover how to create an effective strategy and plan, including measurable objectives, that will help drive the success of you and your channel partners.

Insights

Effective Partner Communication Starts with Empathy

Discover best practices and recommendations when designing a communications plan, that is sympathetic to the lifecycle of the partner program.

Insights

CO-OP Versus MDF Funding Models

Find out more about the advantages and disadvantages of CO-OP accrual and MDF proposal-based funding models.

Insights

Channel Rewards Programs for the New Digital Transformation Era

Learn how to modify sales processes to align with the new, digitally connected buyer’s journey, with points-based rewards incentive programs.

Insights

Maximize the Effectiveness of your MDF - CO-OP Program

Discover five best practices that can be utilized to improve the effectiveness of your current or new MDF program and improve time to revenue.

Insights

Opportunities to Optimize Partner Engagement

Achieving partner engagement success requires getting personal with your incentive program. Learn how to deliver an exceptional partner experience.

Insights

Channel Rewards Checklist for Today’s Marketplace

How to create a successful channel partner rewards strategy & ways to drive partner behavior that aligns with market evolutions & growth strategies.

Insights

Partner Prospecting and Onboarding

Utilize this onboarding checklist to successfully recruit the right partners with business models and skills aligned with your company’s objectives.

Insights

Promotional Allowance Program Regulations

Download this best practice guide, that explains the promotional allowance program regulations and how they impact MDF / CO-OP programs.

Insights

Starter’s Guide to Finding an MDF/CO-OP Solutions Provider

Utilize this services checklist to assist in finding your best matched MDF/CO-OP solution provider and ensure alignment with business objectives.

Insights

These Trends Are Changing Channel Marketing

How channel marketers are adapting to the changing channel landscape and trends affecting partners and their businesses.

.png?width=992&height=620&length=992&name=e-book_Rebates%20Reinvented%20Best%20Practices%20Guide_Thumbnail%20(552x%20346).png)

Insights

Rebates Reinvented Best Practices Guide

This guide will teach you how to develop and run a rebate program that can take your marketing to the next level.

Case Studies

Healthcare: Pharma: Points Based Reward Incentives

Centralized healthcare stakeholder community portal, engaging professionals for their insights with survey participation, by points-based reward incentives.

.png?width=992&height=620&length=992&name=e-book_The%20Ultimate%20Guide%20to%20Points-Based%20Channel%20Rewards_Thumbnail%20(552x%20346).png)

Insights

The Ultimate Guide to Points-Based Channel Rewards

How vendors - and their sales channel - can engage with Points-Based Rewards to modify sales processes and align to the buyer’s journey.

Insights

Maximize Rewards For New Digital Era

Discover insights into digital transformation and how vendors and their channel can align to the new buyer's journey with a Points-Based Rewards program.

Case Studies

Technology: Data Solutions Provider Points-Based Rewards

Points-based brand advocacy and enablement program, empowering channel partners to accelerate sales growth and improve technical knowledge.

Insights

The Three A's of Strategic Partners

Want a successful partner experience? Use the Three A's Criteria to identify and evaluate your strategic partners and focus your energy effectively.

Insights

HVAC Guide to Finding an MDF/BDF Solution Provider

The HVAC industry is facing a huge opportunity to leverage digital automation to improve efficiencies. Start by finding an MDF/BDF Solution Provider.

Insights

Optimizing Automotive Aftercare Dealer & Distributer Engagement Points-Based Incentives

Points based incentive programs are an effective way to drive automotive aftercare dealer and distributor engagement. Learn how to motivate revenue-generating behavior, and increase sales.

Case Studies

Technology: Points Based Program

This global IT vendor increased loyalty, motivated their reseller network and grew sales by 10% YOY through points-based rewards and incentive travel.

.png?width=992&height=620&length=992&name=e-book_SUPPLY%20CHAINS%20HAVE%20CHANGED%20FOREVER-%20How%20brands%20can%20engage%20and%20motivate%20resellers%20for%20joint%20success_Thumbnail%20(552x%20346).png)

Insights

Supply Chains have changed forever: How brands can engage and motivate resellers for joint success

Nimble brands are changing how they work with suppliers & resellers to optimize manufacturing, inventory, distribution, partner engagement, & motivation.

.png?width=992&height=620&length=992&name=e-book_Ecosystem%20Orchestration%20Has%20Landed%20and%20is%20Here%20to%20Stay_Thumbnail%20(552x%20346).png)

Insights

Ecosystem Orchestration Has Landed and is Here to Stay

With today’s increasingly complex channel ecosystems, how do you get the most out of your partners, resellers, suppliers, providers, and influencers?